Around a year ago, old-school Tip of the Week had a “2025 Enshittification: part 1” post which looked at how online services routinely drop features that people like because it suits the provider to not sustain them. It’s high time to revisit the topic, specifically looking at changes being made to online mapping services and one popular document scanning app.

In truth, if you’re going to rely on a free service, be ready to expect the provider to muck it up for you. If you like to look at your old house on Google Street View, best head over there now and screengrab it as some day they may decide to stop storing previous captures or something.

It feels like it’s only a matter of time before Amazon starts making Alexa a paid-for service, or subsidises free use for telling you the weather or play the radio by playing “would you like to buy a new Carlos Fandango umbrella to protect you from tomorrow’s rain?” inline ads.

Microsoft Shutters Lens

A bit niche, maybe, but Microsoft has been offering a scanning app for smartphones for years. Originally called Office Lens and available for Windows Phone since 2014, later rebranded (of course) Microsoft Lens and even gaining “PDF Scanner” to tell you what it’s primarily for. It was previously discussed in old ToW #682. There used to be a PC app as well as iOS and Android ones, but that has gone already.

Despite nearly 1M ratings of average 4.8 and over 50M downloads on Android, its days are numbered. Rather than keep Lens alive, Redmond has decided to build some of its functionality into other apps, like OneDrive and/or OneNote. Sadly, neither is as simple, fast or fully-featured as Lens is/was. RIP.

Of course, there are plenty of other alternative scanning apps, including the built-in one for Android users, where you just point the camera at something which looks like a document and it’ll give you a shortcut to Google’s own scanning software which can detect page edges, bundle multiple scans into a PDF and so on. Since the scan feature is part of the Files app, you can go there and start a scan directly too.

How many times have you seen a statement like “for your safety and security”, and realized that its primary goal is actually to make somebody else’s life easier?

Google had a neat feature, if you chose to turn it on, where Maps on your phone would keep a record of where you’ve been and upload to your Google account, so you could view your travels within Google Maps on your computer. Called Timeline, it was briefly covered in previous ToWs including the trend for apps to be replacing websites and not always to the users’ benefit.

Timeline was discontinued so you could no longer go to Maps and see where you’d been in the past. It’s tantalizingly still there in the menu today, but all it does is tell you to use the mobile app and offer more help on the activity controls.

The reason? For privacy’s sake, Google was no longer going to store all that info on its servers, rather the tracking data would only live exclusively on your primary phone. Sounds fine, unless you lose the phone and don’t have it backed up, or some other calamity occurs and deletes all the data.

Is this to protect the user? Or is it to protect Google from liability in case its service was somehow compromised, and the whereabouts of millions of people over time had been made available?

The DIY Alternative

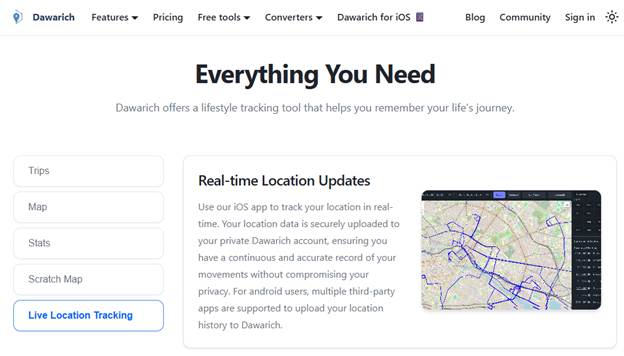

If you like the ability to track where you’ve been, whether that’s to make your mileage claims easier or just to provide yourself an alibi when accused of being somewhere else, there are alternatives to Google Maps / Timeline though none are quite so easy to use. Self-hosting – as in running a server on your own network rather than relying on a cloud provider who might vanish tomorrow and/or start monetizing your data – is a favoured option for tin-hat wearers and honest folk concerned with privacy and/or who prefer to make their own lives difficult.

*easy to follow may be relative to your exposure to config files, IP address mapping etc

Dawarich lets you import location history from Google Maps or you can have apps on your phone regularly tracking and reporting your location history directly to your Dawarich server.

Is Bing Maps really a Zombie?

Sticking on the theme of making mapping stuff worse, Microsoft has been busy “evolving” Bing Maps.

Launched as “Virtual Earth” over 20 years ago, it morphed into numerously named Windows Live, MSN and eventually Bing Maps for consumers as an alternative to Google Earth and Google Maps, and also aimed at enterprises in the hope that they would build mapping services into other applications and pay for the privilege. There had been a previous set of software and services called MapPoint dating back to the Y2K, now superseded.

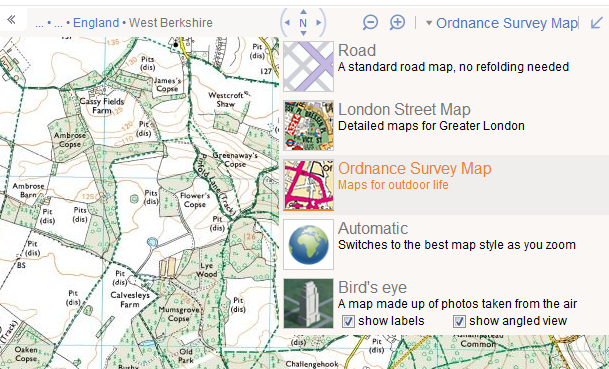

There were some cool features that differentiated Bing from Google when it came to maps – things like high-resolution “Birds Eye” images taken from spotter ‘planes…

Microsoft UK HQ – TVP – in old “Birds Eye” images – note that B5 was still being built, so must be 20 years old?

… to free use (for UK users) of the Government’s Ordnance Survey mapping data. At one point, Bing even licensed the old A-Z maps for London, as “London Street Maps”.

Bing Maps showing Ordnance Survey, with other options including licensed London A-Z Maps

Bing also offered drive-by imagery akin to Google Street View called Streetside. It was never quite as good as Google’s service and it took years to become available internationally, but there were places where it would have more up-to-date pictures compared to Google’s own Street View pictures and data.

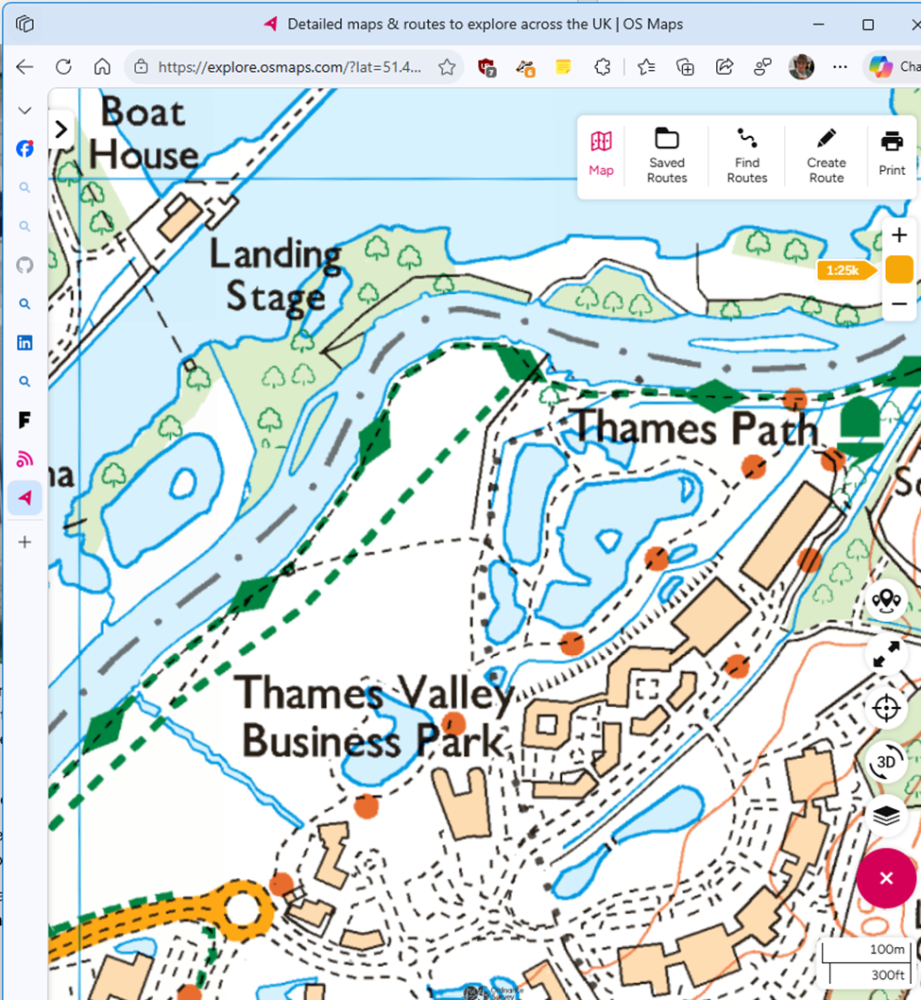

TomTom “surveyed” Thames Valley Park at a time when the park was closed

As you can see from the view above, the images were taken by cars operated by veteran satnav provider, TomTom. Similarly, the Ordnance Survey maps and Birds Eye images were licensed from other 3rd parties.

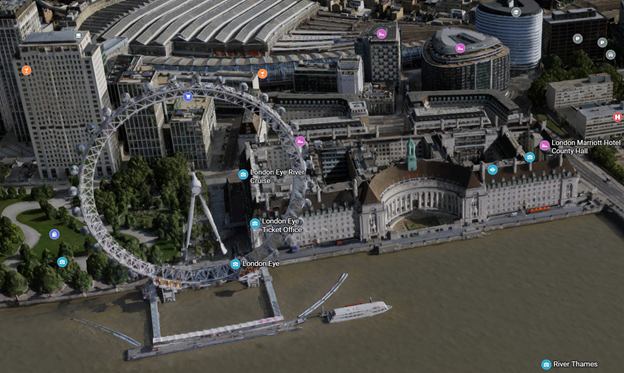

Unfortunately, when a licensing agreement exists then it also means at some point, one or both parties might decide to not continue it. Such has happened with Bing Maps, the consumer offering – it has dropped pretty much everything of interest beyond basic map and satellite views. A 3D option does offer some cartoonish generated models of some areas, though it’s a long way from being universal.

The London Eye in a mock 3D render. Looks OK from a distance but like a 1990s arcade game up close

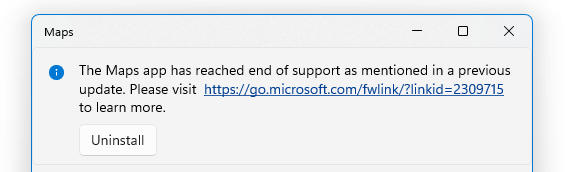

Microsoft also had a Maps app for Windows, which was a wrapper for the Bing Maps service but could also deal with offline data. Presumably due to lack of use, the Maps app has now been taken out behind the bike shed and given a good knobbling:

Nothing to see here, move along, move along

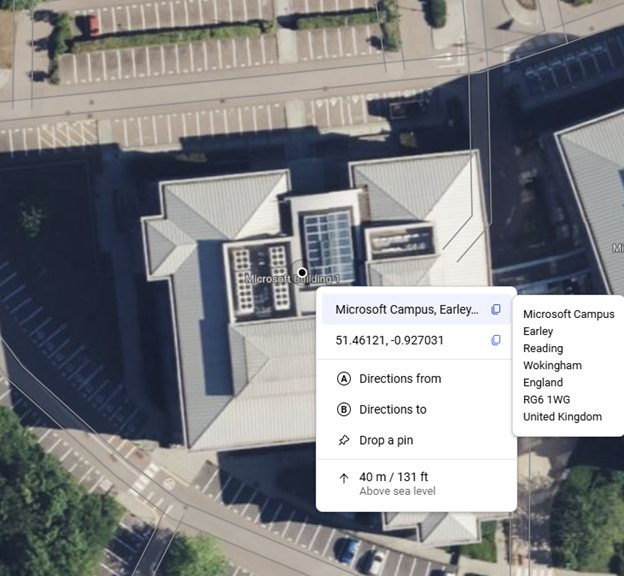

On the plus side, one useful feature which wasn’t present previously, the latest Bing Maps will show the exact address (including Post Code or Zip Code) of any point you right-click on, also displaying the lat/long coordinates and even the height above sea level.

Bing Maps still shows Microsoft Buildings in TVP. B1 is the last remaining one open.

It was announced that Microsoft is shutting down Bing Maps for Enterprise and migrating everything at the back end to using Azure Maps, which has a different set of functionality primarily aimed at developers looking at embedding maps into other sites and overlaying other data onto a map. It’s easy to wonder at what point Redmond will pull the plug from Bing Maps altogether.

Accessing Missing data from Bing

Sadly, there’s nowhere else providing the TomTom Streetside views, nor the Birds Eye images, other than going to Google Maps and seeing what they have.

If you miss the OS Maps feature from Bing Maps, there are few alternatives – the best is probably OSMaps.com, which still offers (for a subscription) what they call topographical maps (i.e. OS LandRanger or Explorer). It’s a little clunky but has a reasonable mobile app too, so you can plan trips and take them offline with you.

Following on from last month’s missive (#783) on internal competition, we’re going to look at a case where it may have successfully spurred a company, and an example of surprising collaboration between erstwhile competitors.

In the 1950s and 60s, clock and watch making was a hotbed of innovation just like the automobile industry and the race for space. New designs and technologies were coming thick and fast. Quartz crystals and batteries were still way out on the horizon, so the Swiss-dominated mechanical watch industry took great pride in building very precise instruments.

Open the back of a mechanical wristwatch and you’ll see many tiny components meshed together to make a little engine that measures out time and moves the hands on the dial appropriately.

An Omega 321 movement, as found in the Omega Speedmaster watches which went to the Moon

Everything is generally driven by a coiled spring which is tightened and powers the whole “movement” as it unwinds in a controlled fashion. Manually-wound watches usually need a few turns of the “crown” on the side, perhaps every day or two. Many clocks work the same way, but with a larger spring might only need a few minutes of winding with a key every month or so.

Though pioneered in the late 18th century, automatic watches (which wind the spring through harvesting energy from the movement of the watch on the wrist) really took off in the early part of the 20th century. If you can see the movement of an automatic watch – either through the see-through “exhibition case” sometimes fitted, or by taking the back off it – it will often have a large “rotor” which swings back and forth as you move the watch on your wrist. You might feel or even hear it moving.

An automatic Rolex 1560 movement from the early 1960s

The rotor signifies that the dreadfully tiresome task of winding your watch every day was dispensed with. But some fancier watches with additional “complications” still had to be manually-wound; perhaps most notably chronographs, watches equipped with a stopwatch function.

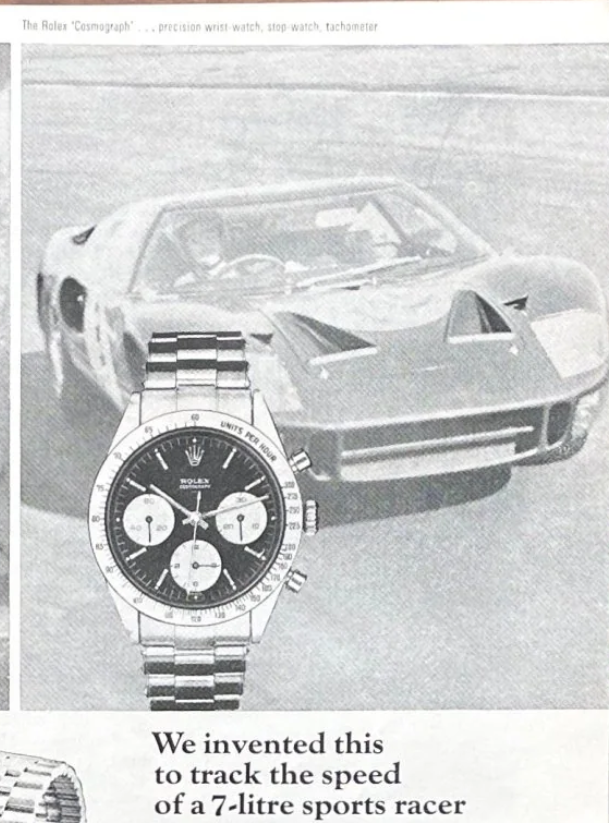

Wrist-worn chronographs (which only show the time, not write it) were popular in the 50s and 60s, especially amongst sporting types, perhaps inspired by famous racing drivers like Stirling Moss, Jim Clark or Dan Gurney.

late 60s Rolex “Cosmograph” advert, egging-up the association with fast cars and watches

But all of these famous chronographs were manually-wound. There was clear demand for the thrusting racy gentleman to have a stopwatch on his wrist that wound itself. Unfortunately, the technical challenge of building such a complicated mechanism that was small and robust enough to wear comfortably was tough.

It was common for watch makers to buy-in the movement they fitted to their watch, just as they’d have the dial made by a specialist, the case fabricated by another and so on. Think of it like a boutique car maker producing a vehicle using an off-the-shelf engine from an external manufacturer. Even major watch producers at the time, bought watch movements from “ébauche manufactures” like Valjoux, Lemania or Venus, none of whom had the resources to dedicate to producing an automatic chronograph. The famous Paul Newman Daytona – auctioned for $15M+ – had a manual-wind Valjoux 72 movement.

So began a famous collaboration between companies that might otherwise be seen as competitors – the watchmakers Breitling, Buren, Hamilton and Heuer got together with Dépraz, who made components for movements, to form what is now known as the Chronomatic Consortium.

Buren had pioneered their own automatic movements which had a “micro-rotor” rather than a big plate half the diameter of the watch. Dépraz had a chronograph module which they figured could be adapted to essentially bolt on to a variant of Buren’s base movement, thus giving them essentially two mechanisms powered by the same spring. In order for them all to fit together, the crown for setting the time had to be on the opposite side to the pushers that worked the chronograph.

A Heuer Carrera from 1969, with the Caliber 11 movement. Note the tiny micro-rotor on the upper right of “HEUER”

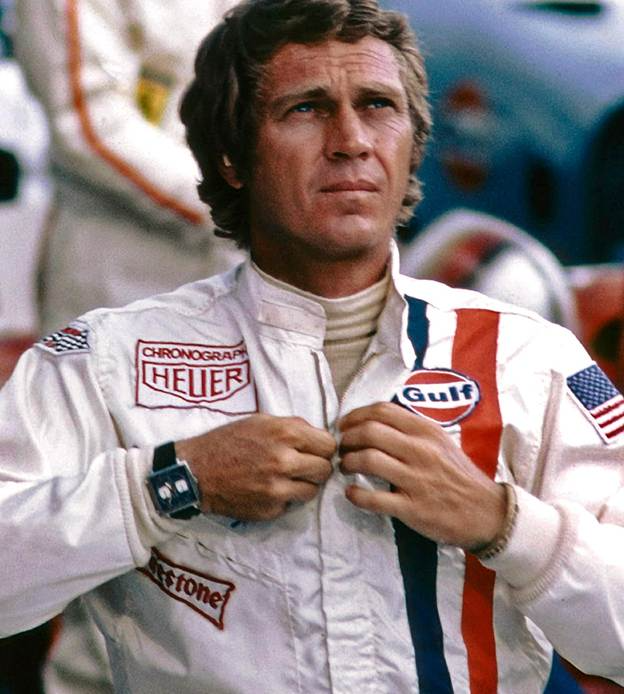

In 1969, Breitling, Heuer and Hamilton (who absorbed Buren during the years of development in the late 1960s) went on to launch ostensibly similar watches with the same basic “Caliber 11” movement within. Heuer’s are arguably most iconic, with the square-cased Monaco appearing on the wrist of the King of Cool, Steve McQueen, in the 1971 film, Le Mans.

Steve McQueen supposedly chose the square Heuer Monaco to match the patch on his race suit

The story behind McQueen’s watch is quite fortuitous; Heuer had a name for sports timekeeping and sponsored various cars and race teams. When McQueen was preparing for the Le Mans film, he said he wanted to look exactly like pro driver Jo Siffert, so donned the same overalls with the big Heuer logo. They also supplied props for the filming including watches.

Heuer and the rest of the “Project 99” / Chronomatic group touted their watches as the world’s first automatic chronographs, though competitor Zenith had been working on their own in-house movement and were so confident they would be first, they launched it in a watch brazenly called “El Primero”.

Even though they’d been working on it for 8 years, and announced it in January 1969, it took Zenith until September ‘69 to start selling their watch, by which time they were more like “El Tercero”, as the Chronomatics’ Caliber 11 was already being sold under several brands, and unseen but coming up the inside on the rails was a company very far from the Swiss cartels, who had designed and built an automatic chronograph and started manufacturing AND selling it in early 1969: Seiko.

Taking on the Swiss

Founded in late 1800s, “Seiko” was in fact several companies under the family of its founder, K Hattori. As Japan opened up to outside trade and competition, Hattori-san started by importing and selling western clocks, jewellery and watches, before starting to develop its own in-house offerings.

After WWII, Seiko developed a diverse range of horological kit – the official timekeeper of the 1964 Tokyo Olympics, Japan’s first Automatic watch, its first Chronograph, first diving watch, even getting into high-end accuracy in watches such that they took the fight to the Swiss on their own turf. There were watch “trials” in Neuchâtel and Geneva in the early 60s, to showcase how manufacturers could produce watches of incredible accuracy. After a few misses, Seiko showed up and started wiping the floor – to the point where the highest profile trials were cancelled the year after. Maybe the Swiss didn’t like getting beaten so took their ball away and went home.

Seiko’s “warring factories”

Revisiting the theme of internal competition, one unusual aspect of Seiko’s approach was to have two completely separate factories, separate companies even, operating to win the same customer. Daini Seikosha, in Ginza, downtown Tokyo, and rural Suwa Seikosha, near Nagano, shared hardly any technical know-how and yet were seemingly pitching similar watches to the same customers. The short version of history is that they were out and out competitors, but a subtler take is that both Daini and Suwa were children of the parent, and expected to treat each other with familial respect, even splitting some tasks occasionally.

A somewhat unlikely source, tech company Atlassian hosts a great series of podcasts on telling stories of team working, and they had a really good 30 minute one from the depths of COVID time, on Seiko’s “Duelling Factories”.

It’s never really been satisfactorily explained why Seiko had two factories that shared so little. There are some examples where a watch developed in one was manufactured – perhaps only for a short while – in the other as well (maybe a capacity issue?), but allowing two separate R&D outfits to develop products that directly compete for the same customer seems like madness to most of us. Then again, look at vintage catalogs, and there are hundreds of pages of barely distinguishable watches, so maybe they just threw everything they could at the wall to see what stuck.

The race for space

The Suwa factory arguably won the race to make the first automatic chronograph; they had 6139-6010 model watches in production from January 1969. When Jack Heuer, CEO of the eponymous company, was exhibiting their first Caliber 11 watches at the Baselworld show in the spring of 1969, Seiko’s president congratulated him on their achievement, electing not to mention that Seiko had built their own, integrated, in-house automatic chronograph and had been already selling it for months, at a fraction of the price of the Heuers, et al.

The 6139 chronograph went into numerous shaped watches over the decade or so of production, famously adorning the wrists of Bruce Lee, Flash Gordon, even making it as the first automatic chronograph in space via the pocket of Col William Pogue. What later transpired is that Pogue’s mission Commander, Jerry Carr, was sneaking aboard a Movado chronograph too. Movado was a sister brand to Zenith, and its watch ran on Zenith’s 3019 PHC “El Primero” movement. So a dead heat to be the first in zero gravity, then.

In the meantime, the Daini Seikosha factory had been working on its own, thinner and slightly more exotic, automatic chronograph movement – the 7016. Sharing no components whatsoever and being of quite different architecture to the 6139, the 7016 was a few years later to market and arguably missed the buzz of its sibling. As such, 701x watches are a good bit rarer.

Seiko 6139-6001 from October1970 – note the Suwa logo below the hands just above the subdialSeiko 7016-5001 “Monaco” from August 1974 – the Daini logo sits just below AUTOMATIC at 9 o’clock

Both movements were integrated, i.e. designed from the outset as automatic chronographs, rather than bolted together such as the Chronomatic Cal 11. The 6139 was the first chronograph to use a vertical clutch, an advanced coupling mechanism now the norm for high-end watches from Rolex, Patek Phillippe and so on. The 7016 has a sub-dial register which counts both hours and minutes, has a horizontal clutch but features a flyback mechanism and was the thinnest automatic chronograph movement for 15 years. The more popular square-ish case shape also leads to its nickname, “Monaco”, after the Heuer model.

Taken from 1972 JDM Seiko catalogs

Maybe they were aimed at the same customer, though the 7016 was around 38% more expensive than an equivalent 6139. Presumably available side-by-side from the same retailer. What were they thinking?

Anyone who has worked in technology has probably dealt with a competitive situation.

Maybe it’s trying to position your solution against all the others companies’ products, perhaps it’s the annual performance review tussle with your so-called “co-workers” or you’re just trying to get funding or investment from the higher-ups to get something done (when they might prefer to spend the money elsewhere). It can be exhilarating and exhausting.

Competing with other external parties to deliver a service or a product probably sharpens the minds of the people developing it, so in theory having strong competitors should make you stronger too (or you don’t survive). But does internal competition improve offerings, make the organisation more efficient, or is just a giant distraction? If “leaders” spend time fighting with each other instead of focussing on the end goal, maybe they’ll eventually lose out to more agile or innovative competitors [See IBM, HP, Digital, Intel…]

Some companies have consciously fostered internal competition or even conflict to accelerate their own developments. Occasionally, companies will pool resources with erstwhile competitors to help them innovate more quickly or to gang up against even stronger companies.

Microsoft and Apple

Both Microsoft and Apple have evolved through several phases from the mid-1970s until now. For Apple, there was the first era of founding Steves Jobs & Woz, then Jobs booted out and Apple nearly going bust, Jobs coming back and saving the world, before Tim Apple took the company to be the biggest in the world.

Microsoft had a parallel of Bill & Paul founding and expanding in the early days of microcomputing, to Windows dominating the OS landscape, Steve Ballmer taking over and laying some of the groundwork for the transformation to being a cloud company that Satya has driven.

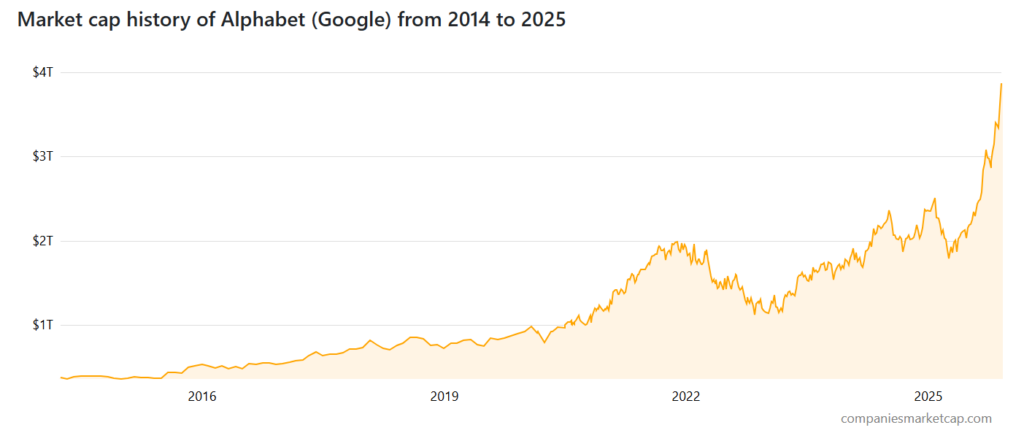

Not many companies get to pivot so many times and still be not just relevant but at the front of their field. They’re still 2 of the most valuable companies ever, by market cap, at time of writing, stocks can fall as well as rise etc etc. Somewhat ironically, since starting to write this piece, Google has overtaken Microsoft for the first time, their value more than doubling in less than 8 months.

Maybe the presence of a talismanic founder or two can help companies in their early stages – in Robert X Cringely’s excellent historical guide to the early days of the microcomputer industry, Accidental Empires (1992), he addresses both Jobs and Gates. Chapter 10, “The Prophet”, starts by calling Steve “The most dangerous man in Silicon Valley”. Bill, in “Chairman Bill Leads the Workers in Song” is characterised as the Henry Ford of the microcomputer industry.

Sometimes, Bill is said to have actively fostered internal competition between different groups rather than imposing a way of doing things – the thinking being that if two or three groups each try to solve a problem then the best solution will win.

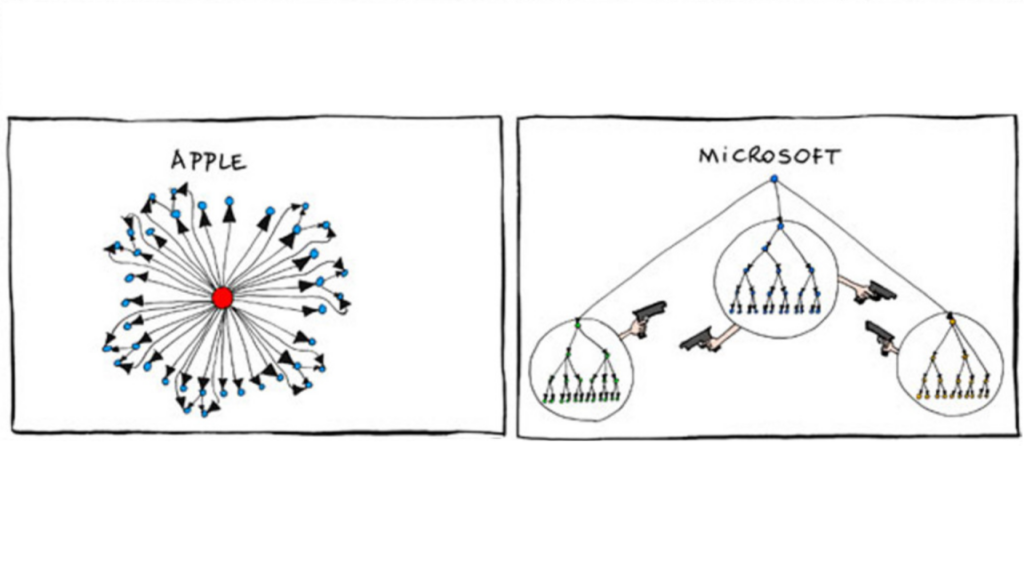

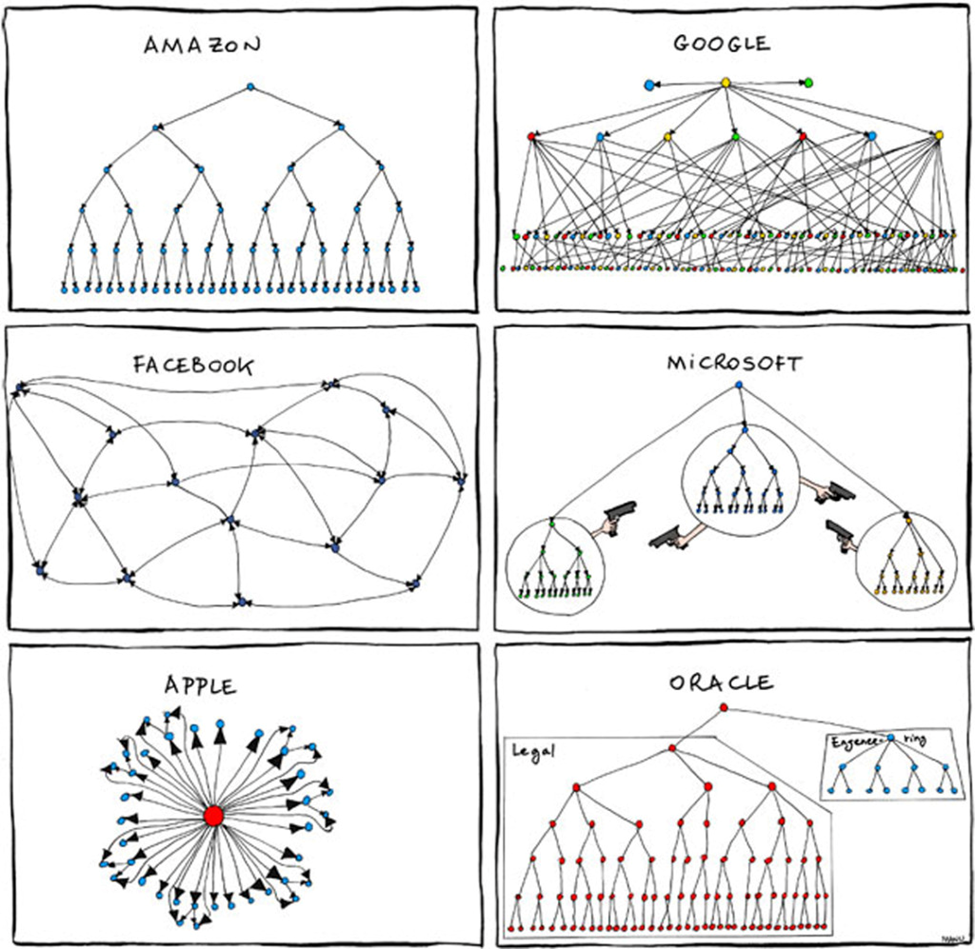

This old joke org chart comparison illustrates a few truisms – at Google, Larry & Sergei might have had the ideas, but Eric Schmidt ran everything. Oracle perhaps spent more on enforcing licensing than on engineering, and at Apple (post 1996), everything revolved around Steve and all decisions went back to him.

But if you were at Microsoft in the early 2000s, you’d smirk with recognition at the warring nature of how their product groups sometimes behaved.

MS: Not just about Windows

For many years, Microsoft had the two cash cows of Windows and Office. The Operating system was licensed to PC manufacturers and sold to enthusiasts and businesses who upgrade every few years. People even queued at midnight on August 24th 1995 to buy a copy of Windows 95; apocryphal stories did the rounds of some shoppers not even owning a computer but they got caught up in the hype for fear of missing something.

Internal influence was rather staked on which part of the division you worked in – Windows, especially under BillG’s tenure when everything else pretty much had to support the Windows business, was the big dog. Office was somewhat secondary but also made Mac versions and was bought by people devolved from whatever cycle they replaced their PC or upgraded its operating system. Server products which ran on Windows NT Server but were tied into usage of Office somewhat straddled the two.

It wasn’t uncommon for Microsoft to have multiple products which overlapped yet were built by different teams – Windows 3.x vs OS/2, Windows 95/98 vs Windows NT, Office vs MS Works, Internet Explorer vs MSN. Even within product groups, there were often numerous bits of technology being developed which had already been built by another team (at one point there were 3 or 4 different and incompatible ways of doing “workflow” processes).

Between 1997 and 2000, the company’s revenue grew from $12Bn to $23Bn but net income nearly tripled from $3.5 to $9.5Bn. What was behind the success? Enterprise software sales. The steady growth of Windows NT and the associated client licenses for running back-office servers, along with SQL Server database and Exchange Server for email was really paying off.

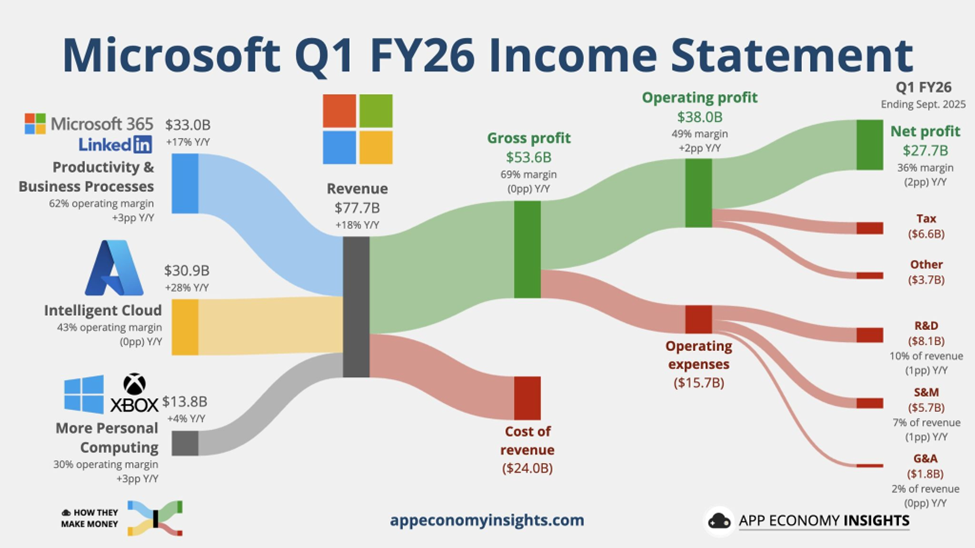

By comparison, Microsoft’s FY25 numbers came out at $281.7Bn with a net income of $101.8Bn – even adjusting the FY2000 numbers using the Bank of England Inflation calculator, the latest figures are remarkable. 2025 revenue is 641% of 2000’s and net income is 561%.

Over time, Microsoft shifted away from just being dependent on Windows & Office, by adding numerous other successful businesses, focusing on Enterprise then the cloud and latterly bunging AI into every offering.

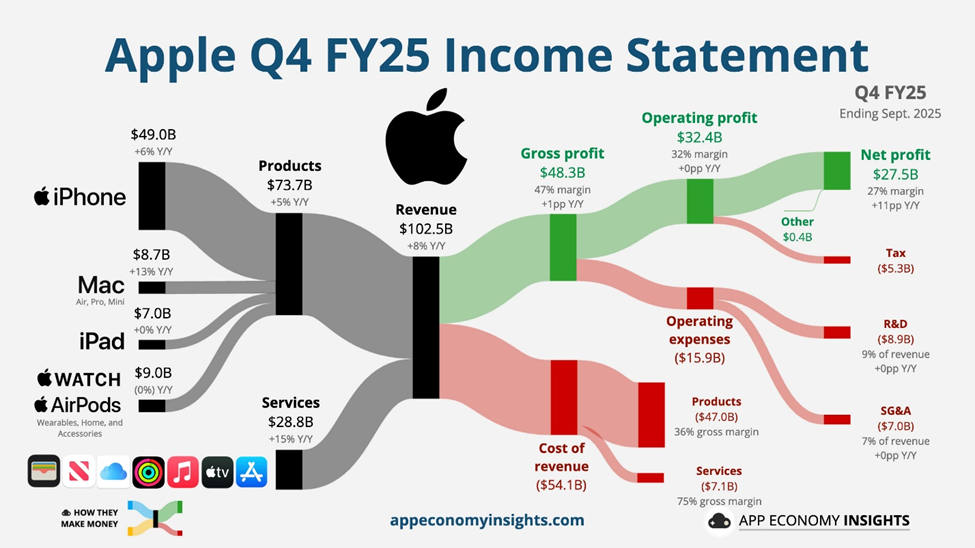

Every quarter when they release fiscal results, Jack Rowbotham posts on LinkedIn summarising where the money flows – and using visuals produced by App Economy Insights it’s quite clear where the power lies now.

Whatever you think of Microsoft, if you cut the company, they bleed software (and services).

Hardware has always been a means to an end – to sell and use the software. The original Microsoft Mouse was just a way to get people used to the graphical interface that would eventually be the key UX of Windows. Today, Surface devices aim to show how a great PC can be and, for now at least, Xbox continues to be the means to sell more games (and Game Pass subscriptions).

Apple – the Return of the King

Microsoft and Apple have had a “complicated” relationship since the early days.

In that seminal interview, Steve lays out his vision for humanity of taking the very best of things to improve itself, casting Apple as true innovators and Microsoft as pedestrian followers.

Jobs famously went to visit Xerox PARC and took inspiration from what they were doing with graphics, mouse, printers and networking as the genesis of the Apple Lisa and later Macintosh products. The Mac has always been a niche offering – arguably beautiful, proprietary and expensive, it could never really compete for the mainstream in the same way that Mercedes or Jaguar or BMW were always going to be in a different league to Ford and Toyota.

The PC and DOS had become hugely successful and when Microsoft debuted Windows, Apple was clearly not happy. Lower-cost, more diverse PCs with many peripheral and software companies building on top of them competed against the Macs with relatively few software packages being developed. Jobs was fired by Apple in 1985. There were attempts to create other products, like the Newton, but they proved unsuccessful and perhaps a costly distraction.

Apple was circling the drain, and at the time of Jobs’ return in 1997, it was said that Microsoft made more money selling Office to Mac users than Apple did selling Macs to Mac users.

Steve Jobs holds an idea that keeps some grown men and women of the Valley awake at night. Unlike these insomniacs, Jobs isn’t in this business for the money, and that’s what makes him dangerous.

Jobs came back and brought in some help from outside – including Larry Ellison from Oracle, despite the boos from the faithful. Steve began admitting that Apple would like to do some software and having software industry expertise on the board might be a good idea.

He also suggested that Apple and Microsoft were going to partner more closely – as a way of resolving some long-time disputes relating to look and feel of Windows and Mac, and Microsoft agreeing to keep supporting the Mac platform with releases of Office at the same cadence of the ones for Windows.

Microsoft was also going to pump some cash in to make sure Apple was kept alive (a useful bet against the Department of Justice, who were breathing down Redmond’s neck at the time). The $150M of non-voting stock that Microsoft bought was sold 6 years later for $550M, so that worked out well.

Jobs made a hugely important point to the Macworld congregation at the time: they need to let go of the idea that for Apple to win, Microsoft has to lose. This idea that competitors can sometimes work together for mutual benefit or even survival is clearly valid.

Apple makes Things

Meanwhile, Apple has gone from near death to world dominance. Jobs led an obsessive focus on customer experience, which made sure they built products that people loved. The iMac injected some pizazz into the ageing Mac product lineup, launched a hugely successful laptop line in PowerBook and MacBook, and came up with a variety of ancillary products like the iPod, iPhone, iPad and Apple Watch. By Q1 2007, the iPod on its own was responsible for almost half of Apple’s revenue.

The iPhone was the true saviour of Apple. For the first time, it attracted new customers to the brand, and they’d go on to buy Macs because they liked the experience (and the integration was well thought out). But it had a difficult gestation: Jobs deliberately kept the development of iPhone separate from the Mac, with direct oversight and freedom for that design team. He fostered direct – sometimes hostile – competition for the software platform to be used in the phone. Either the iPod would grow to become a phone, or the Mac OS X would be shrunk to form a new OS. The latter prevailed.

Looking at Apple’s fiscal makeup today, you can see that the majority of its revenue comes from products like iPhone, but services like iCloud, Apple TV, iTunes etc make up 28% of its revenue but 45% of its gross profit.

If you cut Apple, it bleeds devices and the related experience. They make great hardware which people love because the design and the software that drives it is well thought out. But the profitability growth is really behind the subscription services that provide that experience: nearly 45% of Apple’s gross profit comes from that services line, even though it accounts for only around one quarter of its revenue.

Are they still competitors?

Having been frenemies for some time and outright competitors for years (remember the I’m a Mac adverts? … not sure some of them would make the cut these days), do Apple and Microsoft still see each other as even relevant let alone a threat or opportunity?

Well, Windows still has the lion’s share of the desktop OS, though it’s fallen from around 85% to 65% over the last decade. The key thing is, the desktop has lost its dominance with more people using phones and tablets, and since Microsoft failed to compete in the phone OS and never really built a compelling tablet, it’s even stevens.

In its early days, Apple’s iCloud storage was partly on Amazon’s AWS and partly on Microsoft’s Azure cloud service – in fact, Apple was among the largest 3rd party users of Azure at the time. Reportedly, iCloud moved to Google Cloud and kept on using AWS for some too, alongside massive investments in their own datacenters.

Nowadays, Microsoft pretty much bundles Office in with a subscription so Mac users might not be counted a significant revenue stream on their own. M365 doesn’t care what device you’re using to access its services, as long as you are.

Very significantly, when Satya Nadella took over as Microsoft CEO, Office for iPad and iPhone were quickly released. Some commentators incorrectly attributed Satya’s new openness (Linux on Azure and all that) to account for the release of Office for iDevices, but the development had been underway for years. Steve Ballmer – who famously faux-smashed an employee’s iPhone – had given it the green light.

So, is internal competition really a good thing?

We can never really be sure.

Having several groups pursuing the same goal is inevitably “wasting” resource, but it may be that without that competitive tension they’d miss key breakthroughs, or fail to challenge long-held assumptions. Recognising and capitalising on opportunity, regardless of how difficult its gestation, that’s what marks out success in the long run.

What Apple and Microsoft have both done is to evolve their missions over time; freed the dependence on one cash cow in order to cultivate others. Just as old dogs lose out to young pups and newly-dominant lions kill the cubs of their predecessors for the survival of their pride, maybe the only way for some companies to survive is to encourage and embrace the “overhead” of internal competition in order to find new business.

Time is relative, man. In practice, since most of us are not rushing about at or near to the speed of light, it feels pretty much a constant, and is something we all too easily take for granted.

The relative importance of the time of day to a caveman would be what time the sun rises and sets, and he wouldn’t really need to define it empirically since all the other things he interacted with would be driven by the same schedule. He wouldn’t care how many hours there were in the day, only that seasons might change and the days would be longer and shorter.

Measuring time accurately and consistently became a challenge throughout human development, particularly once we started to travel around. Manufacturing, commerce, communications and more all depend on knowing what the time is, sometimes to an extremely accurate degree. Even kiddies’ games too.

Where am I?

In the 17th Century, King Charles II* of England, Scotland and Ireland saw fit to create a Royal Observatory in Greenwich, London, in order to keep up with advances in astrology that rivals (especially the French) were making.

Back in 1676, the first “Astronomer Royal”, John Flamsteed, was tasked with finding a way to more accurately navigate at sea. In essence, he began working on the base for subdivision of time zones and for calculating longitude (i.e. how far east or west they are) and therefore help ships not get lost at sea.

The Prime Meridian was defined quite some years later – 1851 – and was chosen (in 1884) as the basis for most navigation systems and the means by which the globe is split up into time zones. East and West is measured in degrees of longitude with the Meridian (and associated Greenwich Mean Time) at point zero.

You can visit the Greenwich Observatory and stand with one foot in the western hemisphere and the other in the eastern hemisphere.

Observing the celestial bodies can help narrow down where you are but to be precise, you need instrumentation which can accurately measure time. In principle, a navigator out at sea could figure out what the time is where s/he was (based on placement of the sun and possibly using stars at night) and could calculate latitude (i.e. how far north or south he or she was).

If there was a way of knowing what the time was at a fixed point, then they could figure out longitude as well, by comparing the current location’s time and the what the time was at, say, Greenwich. Imagine a sailor halfway across the Atlantic – if they know it’s noon by observing the sun but they had a clock set to GMT which said it was 3pm, they could calculate the number of degrees of longitude difference and therefore pinpoint where they are, with at least a degree of certainty.

Unfortunately, accuracy of clocks and watches in the 17th century was pretty woeful – many early timepieces only had a single hand, as they weren’t really accurate enough to measure minutes. Sundials remained the most accurate way of measuring time.

The only clocks which could keep good time needed pendulums to swing and that doesn’t really work when the clock is pitching up and down on the waves, so once a sailor had left port there was no way of them keeping track of time at a known point, only the time where they were now.

Following repeated tragic shipwrecks due to vessels being off course to where they expected, the Board of Longitude was established in 1714, with a generous bounty (several £M in today’s money) promised to anyone could solve the problem.

Clockmaker John Harrison devoted much of his life to building clocks and “marine chronometers” which could prove remarkably accurate, enough to measure longitude over a long sea voyage. One test, by King George III no less, measured accuracy within 1/3 of a second per day over a 10-week period, and Captain Cook took a replica of Harrison’s H4 clock to his second voyage down under. They were expensive – about a third the cost of the ship – but if they helped avoid catastrophe, they were worth it. After much shenanigans, Harrison finally received the Board of Longitude’s payout when George III* personally intervened.

You can take a guided tour of the Observatory, seeing some of Harrison’s clocks and telling the story of what a massive impact solving that tricky problem had, seemingly trivial in today’s world: how knowing the time can help to pinpoint where you are.

You might even be lucky to be guided by former Master Mariner, John Noakes,who now volunteers at the Observatory. A life spent selling strategic software solutions has not dulled his enthusiasm for the subjects of seafaring, navigation and time.

The Royal Observatory played an important part in setting the time for ships, too – at exactly 1pm every day, the brightly-coloured Time Ball drops and any ships within sight of the Observatory could adjust their own clocks to make sure they remained accurate.

There was even a family – culminating in spinster Ruth Bellville – who “sold time” by taking a 1794 chronometer pocket watch and regularly setting it correctly from Greenwich. First her parents and then Ruth would journey around London, showing the watch to their clients (clock and watch makers, or other businesses) so they could accurately synchronise their own clocks to be within a few seconds of Greenwich Mean Time.

From the Clockmaker’s Museum, at the Science Museum, London

Despite availability of radio technology and even the Pips, it’s pretty remarkable that as late as the 1940s, people were still giving money to an old lady toting around a 130+ year old pocket watch, just to have a look at it.

(c) Viz, 1990

19th and 20th Century Time

By the early 1800s, it was common for towns in the UK to have clocks in their church or town hall, and that was the reference for things of local importance, like what time the marketplace opened. Those clocks would be set by the midday sun so they would be more-or-less correct.

The problem is, noon in (say) Bristol might be 6 or 7 minutes later by celestial time than it is in London, and that made things difficult when trying to operate between the two, such as making a railway journey according to a published timetable.

Great Western Railway was the first, in 1840, to adopt a universal time standard set by Greenwich, which meant if you were catching a 2pm train in Bristol, it would be 2pm London Time even if a clock in Brissl said it was still 1:53.

Despite some resistance from red-faced locals complaining of interference from the capital city, it wasn’t long before everything across the country became synchronised to GMT and the idea of locally-defined time went away.

From grandfather clocks and pocket watches, by the mid-1900s, wearing a wristwatch became more the norm for gentlemen. Well-to-do ladies may have had a bracelet watch for some time, but it was during the Boer War that soldiers started routinely strapping a small pocket watch to their wrists so they could easily coordinate actions. It didn’t matter so much what the correct time was, so long as they all had their watches synchronised on the same time.

During the mid to late 20th century, the development of electronic time keeping made it much easier for people to know what the accurate time was. Atomic clocks were developed to measure down to tiny fractions of a second, and even redefined the international standard of “a second” as being based on the vibrations of a particular atom.

Scientists have even proved Einstein’s theory of relativity applies, by raising one of two atomic clocks by 1 foot in height, and seeing how it sped up ever so slightly. It’s only 90 billionths of a second faster over the span of a human lifetime, so tall people really needn’t worry about ageing quicker.

Further Watching and Reading

Futurologist Ray Kurzweil proposed in 1999 that the rate of innovation is itself accelerating, so that the first 30 years of the 21st century would see the same or greater technological change than all of the change from the 20th. Some of Ray’s predictions are a bit whacko, but consider that the 20th century itself gave us flight, adoption of mass transit and telecommunications, the transistor, electronic computers, the internet…

… so how have the first 2.5 decades of 21st C gone so far? Smartphones, social media, online shopping, Google Maps, the human genome… Right enough, by 2030, we may yet be supplicant to fuelling the AI overlords.

What’s the time now?

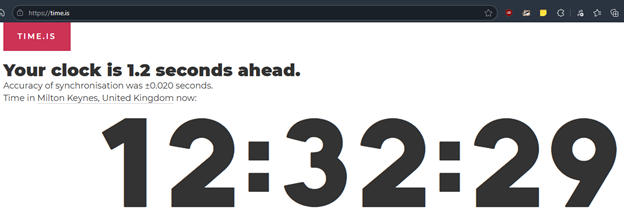

Using your phone or computer, if it keeps its clock set to the network it’s attached to, is probably the most accurate way of telling the time. Try going to the website https://time.isif youwant to check how close you are, really.

If you have Amazon Prime, there’s an interesting documentary, The Watchmaker’s Apprentice, which tells the story of George Daniels, arguably the greatest watchmaker of the 20th century, and his protégé Roger W Smith. Daniels is no longer with us, but Smith still hand-makes watches that will routinely sell for >$1M.

If you can get over the somewhat cloying narration of Gimli/Treebeard, it’s quite an good tale.

This is part 3 of the “Is the car industry doomed?” series, following Part 1 and Part 2.

Looking back through history, government involvement in automobile manufacturing and its supporting infrastructure hasn’t always gone well, though examples do exist of dominant authority proving effective.

From the mid-1920s, the German government decided it wanted to build a network of roads – which became known as the Autobahn. When Hitler took power, he enthusiastically progressed the project and had the idea in the late 1930s of a car for the masses to go with their new road networks, commissioning a well-regarded engineer called Ferdinand Porsche, to make it a reality.

By the early 1970s, the Volkswagen Type 1 (aka “Beetle”) went on to overtake Henry Ford’s “Model T” as the most produced car up to that point, eventually tapping out at 21.5M models over an unbelievable 65-year lifespan. It was eventually overtaken by the Toyota Corolla, which remains at the top with over 47.5M produced in nearly 60 years.

The British Leyland experiment

In 1968, numerous established British car brands merged with the goal of being able to take on the globalising American juggernauts like Ford and General Motors, through creating efficiencies, economy of scale and all that kind of stuff.

Sadly, it didn’t go too well and the UK Government had to step in and nationalise the whole thing in 1975, under the “British Leyland” name.

There followed years of industrial turmoil, cars that were less well built or less well received than expected, and eventual dismemberment and sale of key brands like Jaguar and Rover. Government interference may have partly caused the merger to happen in the first place. Eventually it had to get involved in running a business it knew nothing about, in order to save face and thousands of jobs.

Zero Emissions Mandates

Coming back to the present day, before Covid, legislators in the EU (and the UK, which was still part of it at the time) decided that in order to reduce emissions and enthusiastically champion the kind of growth that Tesla was starting to experience in the US, they should encourage the car industry to invest in a transformation to electrification.

So, governments started offering incentives to offset the additional costs for end users, through direct subsidy to consumers, grants for installing home-chargers and tax breaks for companies supplying EVs to their staff. They also invested in improving public charging networks and ultimately legislated to force car companies to reduce emissions and speed up the uptake of EVs.

The European Union, however, did set out rules that meant it would no longer allow the sale of petrol or diesel cars after 2035, with stringent targets to reduce emissions of Internal Combustion Engine cars ahead of then. The EU threatens to penalise car companies based on the average CO2 emissions of their sales – though a reprieve has been granted for now.

Car companies reportedly considered restricting the numbers of its most polluting models, dropping certain ICE configurations altogether to avoid selling too many (and racking up fines by the resultant raising of their average CO2 output). In some ways this is what the legislators want, even if that means the highest performance cars in the range (such as Porsche’s 911 GT3) have to be restricted in numbers, even if the demand is there to sell more of them.

The UK government in 2020 decided that they would accelerate the move to EVs, and ICE vehicles would be phased out by 2030. That has now been relaxed to keep in step with the EU, given than the global car industry would be targeting the 2035 date for compliance anyway.

The current US administration quickly tore up the environmental restrictions due to take effect from 2027, so for now it’s perfectly OK to keep on buying the mix of pickups and SUVs that seem so popular.

The best selling “car” in the US is the Ford F-150, which will do about 14-17mpg in real world driving, emitting around 250 – 350g/km of CO2 (in the European model) depending on engine size.

Forecast demand for EVs is picking up but it’s still a long way from being the dominant form of propulsion. They are often more expensive to buy than traditional ICE cars, even if the running costs over time might be lower. Residual values have so far been poor – headlines saying that EVs lose half their value in 2 years could be enough to give buyers the jitters about buying a new, premium electric car.

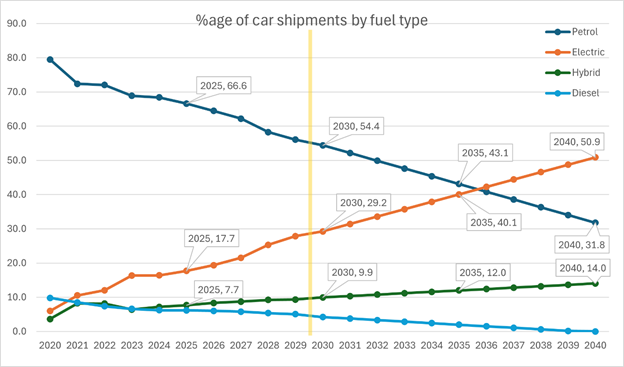

Analyst Statista provides data with forecasting until 2029; taking a straight-line extrapolation (which is unrealistic but serves a purpose) from 2030 to 2040, would conclude that even by 2035, Petrol shipments would still have the upper hand.

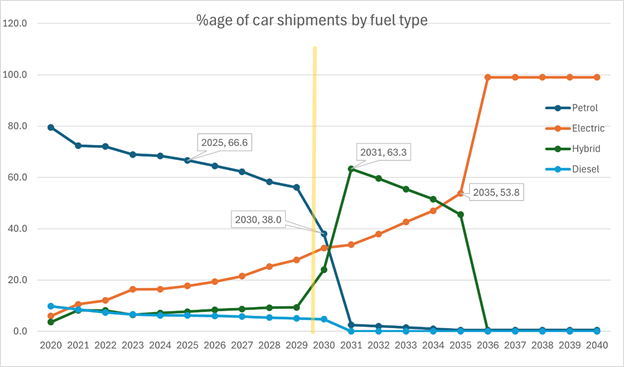

If government mandates and incentives keep being offered or even increased, it’s likely that EV uptake will accelerate. If we assume that pure petrol and diesel will to all intents dry up post-2030, and that there’s at least a bump in hybrids for a while before them being essentially unavailable after 2035, maybe it would look like …

In truth, it’s unlikely that diesel, petrol or hybrid will completely stop in 2030/35. Even if the EU keeps its restrictions in place, there’s no telling what the US might do, or what will happen outside of these major blocs. We’d assume that pretty much all petrol and diesel will become MHEV or PHEVs, and for a while at least would continue to out-sell EVs.

Some car manufacturers bet the farm on EVs – take, for example, Geely. Amongst various Chinese domestic brands, they own Sweden’s Volvo & Polestar, the London taxi company and former UK sports car maker Lotus. Polestar used to be a sporty sub-brand for Volvos, like Mercedes’ AMG or BMW’s M-division, but it spun out as a separate company initially offering a high spec PHEV before launching a range of BEVs.

Even with government assistance and tax penalties on more polluting cars, it seems people aren’t rushing to spend £100K+ on a 2.5 tonne luxury electric SUV. Lotus also joined the breathless pre-COVID rush for EV hypercars that would produce crazy power and cost millions of pounds. It seems the uber-rich don’t much want them either.

For driving enthusiasts, even buying new ICE cars – in Europe at least – also comes with the downside of a variety of mandatory safety features. On the face of it, more safety = better, but the new GSR2 regs require a variety of systems (like speed warnings) to be enabled every time you start the car, which means the car beeps and bongs for a variety of reasons, and can take many menu options to deselect the features.

Ironically, with the trend to replacing physical buttons with screens, the driver-monitoring camera on a modern car will tell you off for not keeping your eyes on the road, just because you’re trying to change the cabin temperature on the big screen whilst moving.

Car journalists talk about “peak car” being 8 – 12 years ago; stuff that has come out since is often more complicated, more expensive and not as nice to drive, even if they’re supposedly safer and better for the environment.

Will legislators blink?

It remains to be seen whether the powers-that-be will continue to try and make the industry switch fully to EVs. The use of tariffs by the Trump administration might stymie imports from overseas, but there’s little incentive for domestic US automakers to fully embrace EVs or even make their existing gas guzzlers super-efficient – Tesla being the notable exception. At least for now, tariffs are also restricting some cars from being sold in the US, as they’d just be too expensive – Volvo’s new Chinese-built ES90 “saloon” being one example.

In the early 2000s, the UK government (among others) incentivised diesel cars as a more efficient and less polluting (from a CO2 perspective) alternative. Fast forward a few years, and diesel particulate and NOx emissions were recognised as being a health danger and the naughty car companies were cooking the books (“Dieselgate”) when it came to emissions testing. It’s just over 10 years since the United States EPA raised its concerns about emissions not being reported correctly.

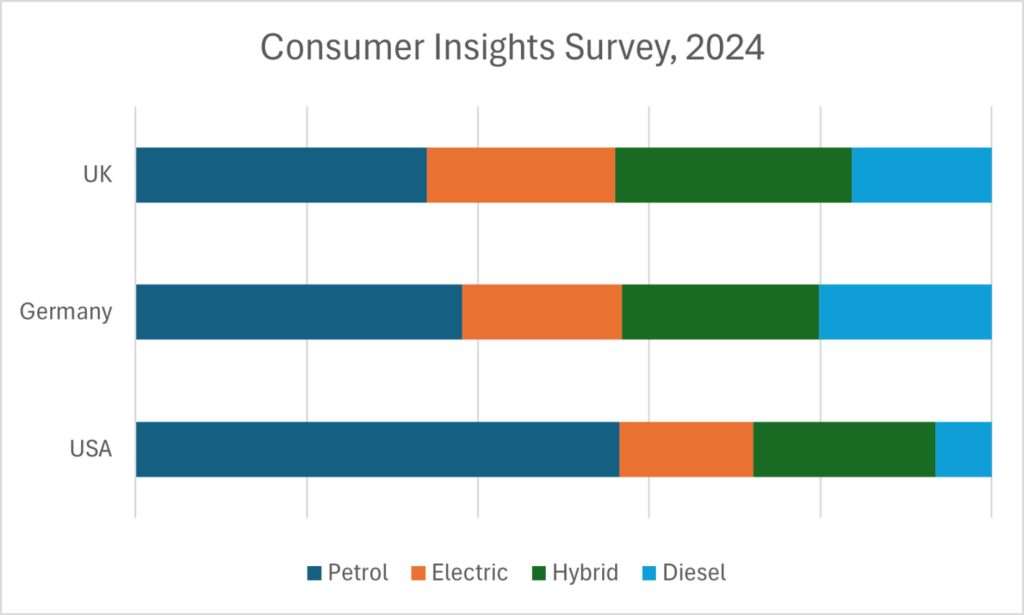

According to the Consumer Insights Global Survey, when asked in 2024, US buyers were 69% looking at Gasoline/Petrol, 19% Electric and 26% Hybrid, with Diesel accounting for only 8% (clearly, each consumer might be considering multiple options since the numbers don’t add up to 100%…)

Germany looked a little more positive, with 53% evaluating Petrol, 26% Electric and 32% Hybrid (though a stalwart 28% still want Diesel, it seems). The UK was 48% Petrol, 31% Electric, 39% Hybrid and still 23% Diesel.

Even a decade before we’re expected to switch to EVs, with these patterns in consumer demand, it feels like we’re going to get a lot of hybrids before we go fully electric, if that indeed happens.

The threat from China

The Chinese market has evolved over the last 25 years; at one point, it was the new nirvana for Western brands as newly affluent Chinese consumers wanted to snap up luxury products from Europe and the US. Auto makers rushed to set up manufacturing facilities in China to serve the growing local market, even producing specific models (like Audi launching the A6L long wheelbase for people to be driven around in).

If the world’s car market is pivoting to be largely if not entirely electric, then BYD and similar brands could be the dominant maker of EVs, even if they have to spin up factories in other parts of the world to sidestep tariffs and other blockers.

Even though the charging networks are more advanced in China than in many other parts of the world, consumers are still worried about range and charging times. This has led to the development of waves of “NEV” – New Energy Vehicles – which are fundamentally electric but not exclusively so. Petrol-powered EREV – range extender EVs – are gaining ground and may become the default since they appear to offer all the benefits of EVs but can run for hundreds of miles.

If Europe and the US are going to still have an automobile industry in 10 or 20 years, they will need to compete with imports from China that are potentially much cheaper, and due to experience and scale, will probably be better than the ones coming from established western auto makers.

So, is the car industry doomed?

Well, obviously not entirely – but the constituent parts of it in a decade or two might be very different to what we’ve got used to over the last 30 or so years. German hegemony at the premium end of the market is certainly looking under threat.

BMW led with innovative electric offerings in the i3 and i8 of 2013/4 but fairly quickly realised they were not going to have true mass-market appeal. It’s taken them years to evolve the rest of the range to offer competitive BEV offerings, but they are now leading the field in Europe (even before Tesla’s sales were negatively affected by it’s CEO’s behaviour).

VW/Audi have had a difficult time, too – early software problems and a poor UX left mainstream buyers waiting (maybe the old adage of not buying anything from Microsoft until v3 also applies here), and they might have struck the crossbar above the open goal of the appeal of an electric Golf replacement when the ID.3 was first launched.

So far, the Chinese manufacturers are grabbing market share by selling good-enough BEVs at a price that beats the premium offerings from Germany, and undercuts the alternatives from US, Japan and Korea. Renault has scored a hit with its cutesy R5 so there is hope from within the established industry that they can make a product that buyers want.

Time will tell if that’s enough to save the existing car makers or if they’ll be replaced by a new wave of names from China and elsewhere.

Car manufacturers have been working on the assumption that soon, they will only be selling hybrid and then fully electric vehicles (EVs). Given that the gestation of a new car model is measured in years if not decades, they’ve been pouring $Billions into developing new car designs, new software platforms and new electric drivetrains. They need to skate to where the puck will be, which means there’s a lot at risk if they get assumptions and forecasts wrong.

Initially, some makers offered EVs as an alternative to the pure internal combustion engine (ICE) in existing models – hence you’d see different versions of similar-looking cars being sold, some with just ICE, some with a hybrid of ICE and electric and some with just Battery Electric (BEV). Volvo offered its XC40 in 2021 with 4 different petrol engines, 2 plug-in hybrids, 2 diesels and an EV option. Prices ranged from £25K for the most basic petrol T2 to £60K for range topping electric P8.

Abbreviation soup*

The purest EV/BEV is simply a car that uses one or more electric motors to propel itself. Power probably comes from a large, heavy lithium-ion battery that can take hours to recharge. Public fast-charging stations are springing up but can be complex to install (given the power requirements they need from the grid), and are many times more expensive to use than domestic electricity costs.

The industry keeps playing with other charging solutions such as swappable battery packs (like old laptops used to offer), or hydrogen fuel cells which generate their own electricity, dispensing with the battery but needing to find ways of getting the notoriously tricksy hydrogen on board.

As technology has matured, existing car companies evolved their ranges by launching new models that were designed specifically as EVs, so could be different to traditional cars in layout.

Mild Hybrids (sometimes known as MHEVs) are easiest to engineer, since they have a small electric motor and battery combination that may just provide additional oomph to the existing ICE, so don’t necessarily have the ability to run on electricity only. They can help the engine be more efficient but don’t replace it in function.

These have been around for years, in various forms – the first outside of Japan was launched 25 years ago, the Honda Insight.

2001 Insight, 80g/km, 1L/3cyl and 87bhp, 85+mpg | 2007 Audi, 322g/km, 4.2L/8cyl and 414bhp, ~20mpg

Honda was just showing what was possible if engineers tried really hard to be efficient. Volkswagen did it 10 years later, with the XL1, and various other manufacturers tried, but the most ultra-efficient cars were never really mainstream. Nowadays, Mild Hybrid (or “Self-charging Hybrid” as Toyota calls them) are the easiest way for manufacturers to add some electrification to an existing car platform.

Plug-in Hybrids (PHEVs) try to offer the best of both worlds – a decent sized battery and an electric motor that could drive the car for maybe 50-60 miles, with a reasonable ICE there to provide longer range and more power. On the face of it, PHEVs are the perfect compromise – no real “range anxiety” of needing to charge the car when on longer journeys, while all the pottering about near home or even short commuting can be done like an EV and charged cheaply from home with a plug-in wall charger.

But there are downsides – when the PHEV runs out of electricity, it’s running just like an ICE car, but it’s got a 200kg-ish battery to lug around. When it’s on EV mode, the battery might be a lot smaller than the three-quarter-tonne affair you’d find in a Tesla, but it’s now got the anchor of a passive ICE to make it less efficient, and the motor is probably not as powerful as a pure EV car would have.

Clearly, we have the complexity of both systems to deal with, meaning there’s also more that might one day go wrong.

There’s also a generally unspoken concern about PHEVs – drift up to a roundabout in EV mode and give the accelerator a boot to get in with the flow of traffic, or sweep down a motorway slip-road in EV mode and put your foot down to get up to speed, and you might cause the ICE to fire up and join the party. In principle, that’s great – more ICE power when you need it, and after a while it’ll shut down to let you cruise along in EV mode again.

But what if that ICE hasn’t had the chance to warm itself up yet? If it was a regular car, its oils and seals and things would ideally have been ticking over for a while before being asked to perform at max power.

If the PHEV had been wafting around on electric drive before arrival at that first roundabout, then the driver demands a slug of power that the EV bit can’t deliver, the car is showing the same kind of mechanical sympathy as starting it up from cold and then jumping straight on the power at thousands of RPMs. Sure, the engines should have been designed and lubricated for this mode, to some degree, but who knows what this kind of “duty cycle” will do for long-term reliability.

Finally, there’s another variant that might become more prevalent than PHEVs – the EREV or Extended Range Electric Vehicle. The earliest example was probably the original BMW i3 REX – it’s an electric car but also has a small petrol motor which is used to top up the charge in the battery, giving it additional range. It’s quite possible that more EV makers will start offering this kind of option as a way of dealing with range anxiety. If they’re allowed to.

*Friend of the newsletter Neil Marley eloquently ranted on LinkedIn recently about the distinction between acronym and abbreviation. It would be tempting to say “PHEV” is an acronym, but it’s an abbreviation. Acronyms are new words like “laser” or “radar”; if you have to spell the letters out (like “WFH” or “EV”) then it’s an abbreviation. Capisce?

Driving EV adoption

Leaving aside the truly experimental, the highly compromised early EVs in the modern era were very much the environmentalist’s choice, before Tesla launched the Model S in 2012 and made them arguably as good as existing car options. Most people – though not all – who drive EVs are won over by their smoothness and technology, as well as the feeling they’re helping the planet.

As it happens, the earliest electric cars arguably pre-date the OG petrol vehicle, but lead-acid batteries and later nickel-cadmium rechargeables can’t hold enough juice for any kind of range. It took the development of lithium-ion batteries in the late 20th century to make a mass-market EV practical, banishing the milk float memories of the 1970s.

GM’s short-lived EV1, 1996-1999

There’s increasing evidence that EVs can last better than expected, better than petrol or diesel cars. With lower vibration and heat cycles running through the car every time it’s used, and fewer moving oily bits and other parts, there’s less to go wrong, and less that needs servicing. Even the brakes might not wear out as quickly since they’ll use the motors to slow the car down: so-called “regenerative braking” is really just reversing the motor to slow the car through putting drag on the drivetrain, also generating & storing electricity for later use.

Electric car sceptics might say that if the average EV is heavier than an ICE alternative, they’ll potentially wear the roads out more quickly, and though they might not be chucking out CO2 and NOx, they could be throwing tyre particles around in greater volume than lighter cars… though that argument is largely debunked.

Whatever, the industry was at an inflection point a few years ago – when should they stop developing or even stop producing “traditional” cars, and instead put all their efforts into the new technology? Eventually, the price difference between the two might go away but at least in the early days, it was not uncommon for EV versions of an existing car to be significantly more expensive.

Charging challenges

YouTuber Harry Metcalfe has covered a few gremlins with relying on public charging networks; if you can find a charger that works, it takes a long time and isn’t necessarily cheaper than petrol or diesel.

If you could charge your EV at 350kWH and it could cover 3 miles for every kW used, a large 100W battery would still take ~25 minutes to fully charge, and might give you 300 miles of range, at a cost of up to £79 from (for example) GridServe.

Compare that to an average petrol car that could do 36mpg, and you could fill a 55 litre tank in a few minutes, giving you 435 miles of range for about £74.

Right now, EVs only really make sense if you can charge them overnight on a domestic tariff at home – but that can only be for a proportion of the population. And taking a 100kW battery from 10% to 100% charge would take 13 hours and cost (for UK users) about £22, or considerably less if they are on the right power plan.

Maybe the ideal scenario for many households would be to have a larger PHEV or EREV for longer trips or carting the whole family+dog+gear around, and a small 2+2 city car for short haul stuff.

According to the UK government’s Office of National Statistics, the 2021 census gave us some interesting demographic information:

23% of UK households have no cars, 41% have a single vehicle and 36% have two or more

21% of households live in a flat. maisonette or apartment.

According to ZapMap, 67% of households have access to a driveway. 9 million households do not, so would need to rely on some kind of public charging network.

EVA England says that over half of existing EV owners who do not have a driveway rely solely on public charging. 60% of disabled drivers reported issues with accessibility in public chargers.

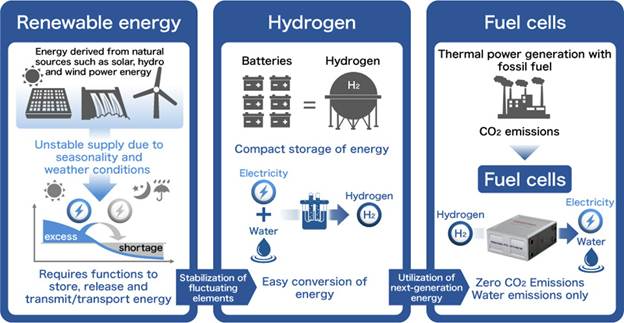

Is Hydrogen the answer?

Ideally, government should get involved to make sure there’s a sensibly-priced charging infrastructure in place, so people living in cities or blocks of flats don’t get disadvantaged when it comes to using an EV. An alternative might be to invest in having a hydrogen filling network, and then car companies could have a different fuel source for powering their EVs.

Car makers have experimented with Hydrogen as an alternative fuel source for years; a fuel cell car can take hydrogen, combine it with atmospheric oxygen to release electrical power, and produce nothing more than H20. It’s also possible to separate hydrogen from water, though it takes a lot of energy to do so – but large arrays of solar panels in a desert could capture huge amounts of power that would otherwise do nothing and split out hydrogen for onward shipment to where that energy is needed.

source: Honda

The challenge with Hydrogen is that it’s somewhat explosive.

Hindenburg airship, 1937

Well, it’s one of the most explosive elements, and can combust at very low concentrations in air. BMW, when making the experimental BMW Hydrogen 7 (which burnt hydrogen in its Internal Combustion Engine rather than using a fuel cell to generate electricity), advised users not to park the car under their house or in fact in an enclosed garage for any amount of time, in case the hydrogen leaked out and blew the whole thing to bits.

While it’s possible to transport hydrogen using variations of the natural gas supply network, it’s not without challenges and speaking with oil & gas safety and risk management specialists, there is little appetite to get involved with it right now. If that could be overcome, a good hydrogen distribution system was established and it became easy to refill your car, then it could provide a useful alternative to the weight and cost of lithium ion batteries and the charging time and range anxieties that negatively impact EV ownership.

A Toyota Mirai hydrogen fuel cell car can add about 5.6kg of hydrogen (at a cost of £10-15 per kg) to its tank in 5 minutes, and that is enough to drive for nearly 850 miles. The Mirai is no featherweight (nearly 2 tonnes) but otherwise is just an electric car in the way it drives, except that it has a compressed tank of gas rather than a big battery. Like Toyota, Honda has been working on hydrogen vehicles for years (including building a joint-venture fuel cell with GM, as used in the hydrogen powered CR-V).

Apart from its tendency for blowing up, the problem with hydrogen for fuelling automobiles is one of the chicken and egg – there are a handful of hydrogen stations in the UK, and the number has been falling, though the UK Gov has put in a bit of funding to add a few more. Without places to fuel up, hydrogen cars are not usable, yet without enough of them to drive demand for a refuelling network, the infrastructure is not viable.

Industrial power

The near-term future for hydrogen power is probably better suited for industrial applications, since the battery electric model is too hard to make work. As it happens, diesel has pretty good energy density – about 100x that of lithium-ion batteries by weight. So, to power an extremely large machine like the Liebherr T284 mining truck (which weighs 242 tonnes dry and has a fuel tank of 5,300L), would need about 500 tonnes of lithium ion batteries.

If you’ve got farm equipment, earth moving machinery or big diggers out in the field, you need them to be running all the time you can – meaning not only would batteries would need to be huge to power those machines on a 12-hour cycle, they would take days and days to recharge.

JCB has been working to build a variant of its diesel engine to run on combusting hydrogen instead. Driving a hydrogen bowser out to the field, connecting it to the fuel tank and filling it up on site makes more sense. Even with the machines burning hydrogen instead of using a fuel cell, it can be a near zero emissions model if the hydrogen was separated using green energy in the first place.

Eco-fuels then?

Another option being pushed by the automotive industry is the use of sustainable fuels. Some mix biofuel with existing fossil fuels to reduce the impact. Some are similar to the hydrogen combustion story with JCB, where if we could manufacture a purely synthetic fuel, then it could arguably be low or even zero emissions in total.

Porsche is investing in “eFuel” which uses hydrogen extracted using renewable energy and combined with atmospheric CO2. When it’s burnt in use later, any CO2 produced is only putting back the CO2 extracted during manufacture.

To some degree, encouraging the continued use of existing fossil-fuelled cars by running them on (more) synthetic fuels is net-better for the environment than replacing everything with EVs. Manufacturing a new EV will add 20-odd tonnes of CO2 to the atmosphere – about the same as driving an average petrol car for 100,000 miles.

What does the future hold?

It’s difficult to be sure, but for now the car industry is still backing BEVs as the answer for domestic transportation. Mass transit like buses or for use in industrial settings, hydrogen looks like a much better option if they can deal with the distribution challenge. It seems unlikely that we’ll be running around in hydrogen-powered cars any time soon.

But there are very real charging challenges with BEVs that make it very difficult to imagine 100% usage. Even if pretty much all new cars are BEVs within the next few years, the average age of cars on the road is already growing – up to (in the UK) 9.5 years, up from about 8 before Covid. If you can charge your BEV at home, it’s great – every time you set off, your car is full of fuel. If you can’t charge at home, though, it’s going to be more hassle than if you’d had an equivalent petrol car.

Perhaps PHEVs or EREVs give us the best compromise, especially if they could be run on synthetic fuel. With a 10 year+ lifespan even PHEVs bought now could still be going strong well into the next decade.

The motor industry – especially in Germany, where it’s about 20% of all manufacturing – is lobbying the EU hard to dilute or even remove targets for transitioning to EVs, citing the relative lack of consumer demand and the huge costs they have incurred in engineering as being an existential threat.

The closer we get to the end of this decade, the more likely it is that governments will capitulate and extend the potential lifecycle of petrol/electric hybrid cars.

The global automotive industry is at a crossroads. Worldwide population growth and demand for cars means some cities are so choked with traffic, you’d be quicker walking. Environmental concerns are driving shifts to electrification while technology intended to improve safety is at risk of distracting and even causing accidents.

Meanwhile, costs have skyrocketed amid worries of slowing consumer demand for brand new cars, leaving industry titans in something of a quandary – they have to invest fortunes to build cars fit for the future. But have they developed vehicles which are too big, heavy and expensive, overburdened with technology that end users don’t want?

What next? Will self-driving autonomous cars become a reality any more than the flying cars vision from the 1950s?

This series looks into some trends, data and perhaps a gaze into the crystal ball on what it all might mean for cars we drive (if we do at all), and the industry which employs 2.6 million people and is valued at $2-3 Trillion annually.

There’s so much to cover, I’ll break it into three parts over the next few weeks.

Part i: “Give the people what they want!”

“Some people say, ‘Give the customers what they want’, but that’s not my approach. Our job is to figure out what they’re going to want before they do.” — Steve Jobs

Steve Jobs is famously attributed as saying this, even though no definitive source has been found. Jobs supposedly went on to repeat the Henry Ford quote that if he asked people what they wanted, they’d say “a faster horse” (which is almost certainly made up).

Jobs was right, at least when new technology is concerned – show them a Mac when all they’ve used is a command line, or an iPhone when they had a Nokia 2110 and you’ll have them hooked. In the car industry, though, things are a little more complex. One thing’s for sure – if you’d asked people in 1996 what they really want, not many would say “an electric car”.

Changing buying patterns

Rewind a generation or two, and consumer habits for buying cars were radically different than today. Every few years, people would change cars by going to the same dealer they always used and probably bought the same brand they always bought. Loyalty was almost cemented in – you were a Ford family because Dad always bought Fords, or a GM/Open/Vauxhall family as Uncle Ted worked in the nearby factory. Switching car brands would be like changing football team you support.

That started to change when established brands like BMW and Mercedes became more attainable and upwardly aspirational. New entrants came into the market offering arguably superior products, possibly cheaper and/or more reliable. Long warranties tempted people to try out otherwise unproven makes. The biggest shakeup, however, came about due to easy availability of finance.

For years, getting a new car on some kind of PCP deal has been the default (for UK buyers at least) – it’s estimated that ~90% of all new and used car acquisitions are financed, though that may be changing. The premise of PCP is that at the end of the agreement, you could walk away, buy the car outright for an agreed fee or, as happens most often, enter a new PCP for a different car. Historically, this last option has been most likely but is softening as higher interest rates bite and the uncertain future residual value of new cars (especially electric vehicles) puts the costs up more.

More people are leasing or taking a new car on a subscription. City dwellers might rely more on public transport and use Uber or a pay-per-use club like Zipcar. Whatever, the traditional demand and supply models are changing.

Long cycles

Cars take a long time to design and build. From early concepts through to figuring out how they could manufacture and later service the thing, to testing for performance in all climates and crash-worthiness, it takes years and costs millions if not billions of dollars.

Add to that the trend in the last 30 years of “platform sharing” – where a car company will build a modular platform that can be more easily adapted to fit different sizes or types of cars in its own range, or even across brands (looking at you, VW, Audi, SEAT, Porsche, Bentley, Lamborghini…). Having to radically update a whole platform let alone the models that it underpins is a very significant undertaking.

Sometimes, car manufacturers try a new model out and it really takes off, so everyone else jumps on the bandwagon. In the 1980s, Chrysler downsized the A-Team sized van to be more of a family run around, and came up with the “minivan” concept, a few months ahead of Renault launching the Espace in Europe. For years, MPVs were wildly popular, before “crossover” vehicles and SUVs started taking over.

Both MPVs and SUVs are examples of users gravitating towards a new format, compared to their old saloons, hatchbacks, estate cars/station wagons etc. What’s the car industry to do? Make more of those, and less traditional cars, if that’s what people want to buy instead. Volvo recently announced that its XC60 is the most popular model ever, supplanting the iconic boxy 240 estates from the 70s. They’ve been threatening the demise of regular saloon/wagons for a few years.

A handy side-effect for the car makers is that they can jack up not just the ride height, but the margins of these larger cars, and that sometimes means others in their range get dumped due to low demand and/or low profitability. Ford cancelled the Fiesta, a small hatchback that was the best-selling car in the UK for years, for these very reasons.

So, the car industry needs to guess what people want a decade before they’ll be in a position to deliver it. They have to deal with legislature demanding better emissions (hence the journey to EVs) and improving safety.

For the most part, great – cars are way more comfortable and safer now for their occupants (though maybe less so if you’re on the outside; research says that if the US replaced all SUVs with regular-sized cars, 17% fewer pedestrians and cyclists would be killed each year). The trouble is all the extra impact protection, safety systems, airbags, screens, cameras, electric seats, 17-speaker surround sound stereo… they all add weight and cost. Cars are on average around 1/3 heavier now than they were 40 years ago, and there are many which are well over 2 tonnes. The largest electric SUVs are knocking on 3t.

Screens and buttons

As well as changing shape of cars and the way people acquire them, another significant trend over recent years has been the prevalence of in-car tech.

The 2020 Honda “e” – lots of screens but still had buttons for some things

Most cars now offer one or more screens to control in-car systems. Consumers now expect Apple CarPlay or Android Auto on new cars (even on relatively budget-friendly ones), though car makers have been dragged somewhat into making them standard fitment – even a few years ago, Ferrari wanted over $4K as an optional extra to enable the tech, even though it was already fitted in the car and it was just a matter of turning it on.

Other manufacturers have tried monetising enabling features that are there already – as the guts of what the car does are increasingly software controlled, it’s easier to just build all the hardware into every car. BMW floated the idea of users paying monthly subscriptions to use certain features, like heated seats – but rightly got some robust end user feedback that they felt they were being ripped off buying a car with functionality present, then having to pay again to use it.

As well as trying to find creative new ways to extract more cash from the end user, car companies have been on a charge to cut costs of manufacture as well – by pushing everything into menus on a screen, they save money from having physical buttons to control stuff like ventilation and heating. They also have a trend for having touch-sensitive “buttons” with haptic feedback, though user feedback is forcing a switch back to actual buttons that enable the user to interact without having to look at the control.

“Simplify, then add lightness”

This quote was attributed – though like all good quotes, it’s difficult to pin down if and when he actually said it – to the mercurial Colin Chapman, boss of Lotus. It’s the distillation of a philosophy that a light car (at least a light racing car) is better. Keeping this simple is also a worthy goal – though in modern cars, it’s more likely that simplicity is a veneer of usability over a hugely complex system underneath. Chapman sailed too close to the wind on occasion when it came to the Lotus racing cars of the 1960s – they were light and simple, but a bit too fragile.

Lightness, however, is a virtuous circle.

In contrast, look what happens when a regular car gets bigger and heavier (because the maker is required to, or if the buyer expects lots of space and bells and whistles inside). It needs a more powerful engine to give it the same relative performance; that in turn might add even more weight and complexity. It will need bigger brakes to stop it, and the wheels will need to be bigger to accommodate them. The tyres will need to be wider to maximise grip, further adding weight and creating more resistance, thus reducing the impact of performance and reducing fuel economy.

This additional “unsprung” weight on each corner makes the car handle less well, so in order to deal with that and all the extra flab onboard, the suspension components need to be thicker and heavier. And so on…

Battery Electric Vehicles (BEVs) face a similar problem – people want a long range (measured in hundreds of miles between charges), meaning they need to fit a large battery (the Tesla Model Y’s battery is apparently over 750kg; that’s more than the total weight of a first generation Lotus Elise).