Motorsports fans the world over are gearing up for another season of Formula 1, where 11 teams will race round and round for an hour or two, in 24 different weekends from now until December. At least that’s true at time of writing – with quite a few races in areas which might be a bit unsafe given recent events, time will tell.

Formula 1 is having a real purple patch – energised by Drive to Survive and the Pittfest F1 movie, the US market in particular is booming, with 3 races taking place there this year. Contrast that to the Americans’ historically lukewarm reception for F1, and the disastrous low point of the 2005 race where 70% of entrants retired before the start.

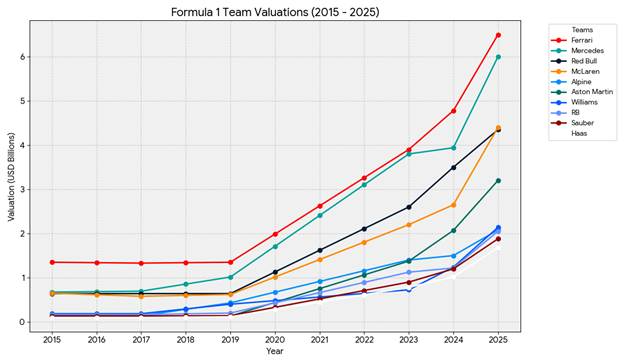

Global audience figures are booming, with younger and more diverse fans, and the teams are increasingly valuable – even the backmarkers are worth billions, with valuations growing by 30%+ between 2024 and 2025.

Cadillac have entered the fray, launching their car livery during the Super Bowl with engines from Ferrari, the factory in the UK and drivers from Finland and Mexico. Not exactly the All American team so far, then, but it’s said they have spent over $1B already and the car has yet to race. They have a goal to grow over the next few years, build a GM powertrain and have engineering excellent at Indianapolis and Silverstone.

New rules – new threats/opportunities

2026 marks a new era in other ways – there are a variety of significant technical changes to make the cars smaller, lighter and more racy while also trying to be sustainable. The fuel being used is 100% renewable, though there’s still the small matter of all the kit that needs to be flown around the world to stage the show…

The radical changes to the cars could shake up the order somewhat – will Lando retain the drivers’ championship or could a resurgent Red Bull bring Max back into play? Can Ferrari’s crazy 180 degree rear wing slip Lewis to title #8…? When the rules all change, the genius of designers taking different approaches to beating them sometimes delivers some unlikely winners – as covered previously with Gordon Murray and the Brabham team, in #778 – Out of the box thinking IRL.

It’s said the driving experience is quite different as 50% of the cars’ power will come from batteries, meaning the driver needs to be continuously harvesting and deploying energy rather than pinning the throttle open and going full tilt all the time he can. “Management” might be the word to describe it, and not every driver is thrilled about that.

75+ Years in the making

Formula 1 celebrated its 75th anniversary in 2025, and despite the fact that the French basically started motor racing (that’s why they’re grand prix, after all) and the governing body, the FIA, is based in Paris, the centre of gravity for Formula 1 and associated motorsports technologies is firmly placed in England. The first F1 race was at Silverstone, and many of the teams have significant bases nearby, even those which are nominally based overseas. The talent pool of engineers and component suppliers acts like a gravity well, meaning if you want access to the best talent and technology, that’s the place to be.

See the map on https://gemini.google.com/share/71467fece82c

Teams have come and gone in the past; it’s an expensive exercise to design, build and operate the cars in a global sport, though some of the best-known names have been around for a while.

Source: Formula 1 on X

Cadillac joins as the 11th team, and Sauber is rebranding as Audi and bravely debuting their own engine too. McLaren use Mercedes engines, even though they arguably compete when it comes to road cars, and Williams also uses Merc.

Since Renault decided to ditch its own in-house engine, Alpine, their sporting brand, has also switched to a Mercedes power unit. Red Bull and Racing Bulls have moved from Honda power and are building their own, with some help from Ford.

Aston Martin hired the most successful designer of F1 cars ever, Adrian Newey, and switched to Honda from also being a Mercedes customer (yet remain so elsewhere, as Aston’s road cars have been using AMG/Mercedes engines for a while). Despite Honda winning recently in the back of a Red Bull, they are arguably a year behind everyone else and the pre-season tests don’t show the Aston Martins in good light.

Ferrari engines power the Scuderia’s own team as well as Americans Haas & Cadillac. In fact, Ferrari is the only team whose cars and engines are developed outside of the UK. The Italian car industry has some symmetry with Britain’s – formerly proud brands competing for the soul of the consumers of the 1950s and 60s have either been lost, swept up inside the likes of Stellantis, or they’ve gone even further upmarket. Ferrari’s cheapest road car starts at over £200K.

The current state of the British Car Industry

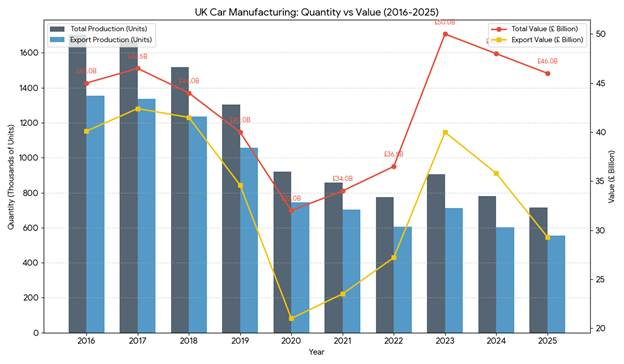

Sadly, if F1 and the wider motorsport sector is doing great guns, the car manufacturing industry in the UK is not in good health. It’s been on the decline for years, decades even, but a combination of the hokey-cokey of US tariffs, electrified competition from China combined with high energy prices, a near-£2Bn cyber-attack, cost-of-living miasma and Brexit, have all conspired to seemingly make things worse. Is it all too late?

In the 1970s and 80s, the UK was quite proud of cars that were made locally – many families chose either Ford or Vauxhall as their brand, and even if some were assembled in Europe, engines and other ancillaries were often built in England. Vauxhall is now part of Stellantis and has shuttered UK production, while Ford has managed to kill off both the Focus and Fiesta which topped the sales charts for so many years. Despite formerly having the biggest car plant in Europe, Ford of Great Britain hasn’t built any vehicles on shore for well over a decade.

Ford is still managing to shift a good amount of its Romanian-built Puma, and Nissan manages to occupy a couple of places in the top 10 with it’s UK-assembled Quashquai and Juke, so it’s not all bad news.

Niche and luxury don’t always pay

Over the years, several British brands have staked their long-term survival on moving upmarket and selling to a more international, luxury or performance focussed crowd. A new “Full Fat” Range Rover starts at over £100K, more than twice what the venerable L322 cost when it was first launched 24 years ago – even accounting for inflation, that’s still 20%+ more. Land Rover has had some good years with international customers, though the devastating cyber-attack which downed production for weeks and its sister brand Jaguar comprehensively scoring an own-goal hat trick as it stopped making cars entirely, to focus on building a £100K+ electric GT, isn’t putting the Tata-owned JLR in particularly good shape.

Sporting cars, for which Britain is somewhat historically renowned (as Mazda recognized when it built the original MX-5 in homage of the 1960s Lotus Elan), aren’t faring much better. Lotus has lurched from one crisis to another for most of its life, and betting big on 2.5 tonne electric SUVs and grand tourer saloons hasn’t really worked. Its Hethel HQ was rumoured to be closing until HM Govt seemingly got involved, but the UK-built Emira sports car that was conceived to take the fight to Porsche is now knocking on the door of a Hundred Grand if you want one that sounds as well as it goes.

While other venerable British sporting brands like Bentley seem to be doing OK by selling luxury barges and Chelsea Tractors, other well-known names are fighting for their lives.

The road car division of Aston Martin is shedding 20% of its workforce in an effort to stop losing money – it’s quite sobering to think they shipped 5,500 vehicles last year but lost £364M – in other words, managed to lose nearly £67K on every car it sold, and that’s on cars that increasingly cost the thick end of £200K.

Ultra-luxury brands like Rolls Royce seem to manage to weather the storm by selling outrageously expensive vehicles to discerning/tasteless & mostly overseas buyers, with profitability increased by heavy focus on pricey and bespoke customization of the cars. Whether the situation in the Middle East puts a long-term dent in their growth remains to be seen.

Clearly, COVID hurt UK manufacturing and it started to rebound but any recovery looks pretty shaky.

Let’s hope that a declining and more specialist manufacturing industry doesn’t inversely follow F1’s gravity effect, by having a brain drain away to the regions who continue to do it well.